Credit scores aren’t built overnight; they improve with on-time payments, good credit history, and low credit utilization. As a beginner, how to build credit from scratch may be a baffling topic for you.

Therefore, here, I’ve mentioned how to build credit fast with or without credit cards, its importance, smart financial habits, and how long it takes to build credit in great detail. Businesses that maintain organized financial records through services like cloud bookkeeping services also find it easier to manage credit and financial stability.

So, stay adherent to this article to improve your credit score.

A credit score is the level of your eligibility to repay borrowed money to the lenders. It helps you assess your creditworthiness quickly, representing your financial stability.

Additionally, improving your credit score can lead to more favorable terms for personal loans, including lower interest rates, higher credit limits, and rewards, ultimately saving you money on borrowing. Proper financial planning, including expert guidance such as CFO services , can also help individuals and businesses manage credit and long-term financial decisions more effectively.

Overall, how to build credit fast helps you to convince lenders about granting you money or a loan.

The main types of credit are revolving credit, installment credit, and service credit. Understanding these forms of credit is essential for improving your financial profile and maintaining organized finances, especially when supported by professional solutions like payroll services that help manage business expenses and employee payments.

Revolving credit is an open-ended loan that allows you to borrow money up to a preset limit, pay back the borrowed amount, and then draw on it again.

Examples: Credit cards and lines of credit.

In installment credit, you can borrow a fixed lump sum of money and pay it back in installments on a regular basis, including principal and interest. Unlike revolving credit, it offers a one-time loan amount for long-term planning.

Examples: Student loans, personal loans, mortgages, and auto loans. When businesses evaluate financing or expansion plans tied to loans or assets, they often rely on business valuation services to determine their true financial worth.

Service credit refers to using essential utilities (internet, phone, and electricity) and paying for them after use. It is similar to revolving credit, where you get the service first and pay the bill later.

Examples: Electricity, gas, water, internet, and cell phone.

You should get your credit card first > pay your bills on time > maintain a low credit utilization score > request an increase in credit limit. These are the ways to build credit scores quickly with a credit card.

Let’s explore these methods in great detail.

Firstly, you should apply for your first credit card after acknowledging the different types of credit facilities.

A secured credit card is a tool that builds your credit score from scratch. It requires a cash deposit as collateral, usually setting your credit limit. You can use this card as your regular credit card, build your credit history, and get rewards.

If you are a college student, a student credit card is a better option for you because it doesn’t require a deposit amount or any credit history, saving you from debt financing. It offers lower credit limits with easier approval, benefits, or rewards, like a regular one.

A hybrid credit card is a perfect blend of a credit and a debit card, allowing you to access funds through your own money or borrow credit to build scores.

Once you have your credit card, make small payments and repay the amount over time to raise your credit score.

The best way to build credit is by paying your bills on time. If you have a credit card, you have a great opportunity to build a payment history via small payments and repay them on time. According to the Consumer Financial Protection Bureau (CFPB), repayment history is the number one factor to increase a credit score.

Maintaining a low credit utilization score means keeping the balance you’re using lower than your total available credit limit. The ideal percentage is below 30%, boosting your credit score by showing you’re not overly dependent on credit and have enough petty cash for daily expenditures.

Examples: If you have a $10,000 credit limit, you should maintain a utilization under $3,000.

After having a credit card for a long time, you can request an increase in your credit limit. It means your card issuer will increase your borrowing cap, which lowers your credit utilization ratio and boosts your score potentially.

Note: If you have a sizable balance, the card issuer doesn’t approve your request. So, it is recommended that you pay down your debt as soon as possible to increase your credit limit.

Building credit without a credit card is possible through installment loans, timely payments, adding bills to credit reports, getting a cosigner, applying for a credit-builder loan, or becoming an authorized user.

Maintaining organized financial documentation through solutions like investment services can also help individuals plan finances better and maintain a strong credit profile. Here, I’ve mentioned these different ways to resolve your problem about how to build credit without a credit card in detail. So, take a look!

Don’t be stressed if you don’t have a credit card; an installment loan could help you build a credit score. Personal loans, auto loans, mortgages, and student loans all establish your payment history, which is one of the major factors contributing 35% to your credit score.

As we mentioned earlier, payment history contributes to the score, so pay close attention to repaying your borrowed money in full and on time. A positive debit and credit cheat sheet and a zero loan balance convince lenders that you are capable of paying your debts.

You should add your bills to your credit report to increase your score. For example, ask your landlord to report your rent payments to the credit bureaus (Equifax, Experian, and TransUnion). These services can add up to 24 months of payment history to your credit report.

You can also include utilities and taxes. Businesses that manage taxes properly through sales tax services often maintain better financial records and credit standing.

If you are not being granted a personal or auto loan under your name, it is advised to get a cosigner (a trusted family member or friend) to help you get approved. Both parties are equally responsible for the debt, and your on-time payments build your credit score.

A credit-builder loan is specially designed to help you build credit scores and savings simultaneously. The lender holds the loan amount, and you should make monthly fixed deposits first. After paying your loan in full, you receive the loan amount along with interest.

For individuals or businesses dealing with cross-border financial obligations or global income sources, understanding tax structures through international tax services can also help maintain financial compliance and stability.

If you are facing trouble getting your own credit card, you can become an authorized user. A primary account holder, whether your parents or friends, adds you to their credit card.

Now, you are eligible to increase your creditworthiness without making payments or having a credit history. However, it is important to note that your score will improve slowly and with limited improvement.

That’s all you need to know about how to build credit from scratch. If you practice these methods, you will surely improve your credit score.

Yes, paying rent helps in building credit, but only if those payments are reported to the major credit bureaus (Experian, TransUnion, and Equifax).

You should use a rent-reporting service or convince your landlord to participate in it. This will help you turn a non-debt expense into a positive payment history.

Overall, it significantly improves your credit score because payment history is crucial for building credit.

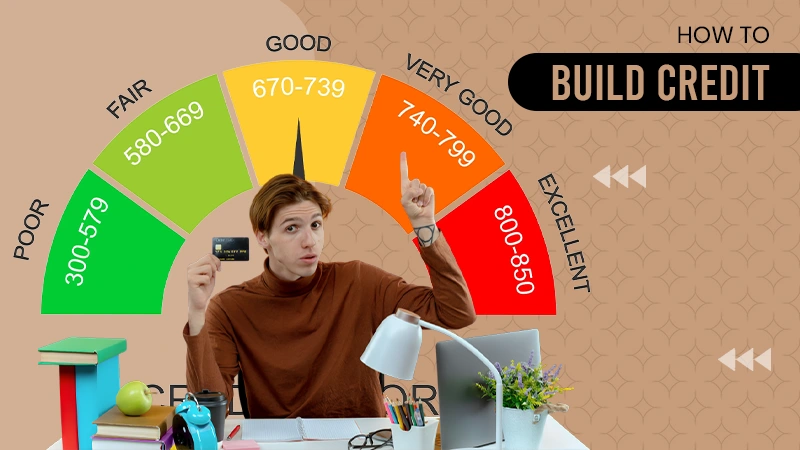

A good credit score is generally considered to be in the range of 670 to 739, according to the widely used FICO Scores.

Look at the breakdown table of the credit score ranges.

| Range | Rating |

| 300–579 | Poor |

| 580–669 | Fair |

| 670–739 | Good |

| 740–799 | Very good |

| 800–850 | Excellent |

Factors like payment history, amounts owed, credit history length, credit mix, and new credit affect your score.

Let’s skim through this section to know how these factors impact your credit score.

Your topmost priority should be repaying the borrowed amount on time and regularly, which is essential in making a good credit history. One single late or missed payment or payslip will negatively affect your credit score. Besides this, if you stop paying the loan amount, this could appear in your credit report and impact your credit score for up to seven years.

Another significant category of your credit data is the total amount you owe, along with current loan balances. It also considers how many accounts you have, balances, and your credit utilization rate to determine your eligibility to pay off debt for your everyday expenses.

Additionally, the age of your oldest account and newest account, and the average age of all your accounts, are taken into consideration. The longer you maintain a good credit history, the better your score improves.

Your credit mix contributes a lot to building a credit score when your report doesn’t have other information. It includes different types of accounts being used or reported, such as credit cards, installment loans, personal loans, and mortgages. This data indicates how effectively you manage and repay the borrowed amount.

Every time you open a credit account, the lender will inquire about your credit reports and all your newest credit accounts. If you open multiple new accounts in a short time, it will result in a greater risk. So, it’s important to avoid opening new credit lines frequently.

You can achieve a good credit score by following some positive habits, such as:

There’s no exact time to make a good credit score, as it takes several months or years of experience if you build from scratch.

In order to receive a FICO Score, you must have:

You need a good credit score for better housing options, paying less to borrow, lower interest rates, and better loan options.

Here are the following benefits of a good credit score for in-depth guidance.

With a good credit score, you have better housing options when you need an apartment for both rent and purchase. Landlords often review your credit report to determine whether you qualify for a rental property.

You may receive an award per month by paying your rent with a credit card, but if you have a poor credit score, you don’t have such an option.

One of the biggest benefits of a good and excellent credit score is paying less to borrow money from lenders. For example, getting a personal loan of $10,000 costs far more with a 500 credit score than with a 700 credit score.

Moreover, lenders or creditors offer low-interest rates to people who have good credit scores, as it signifies reduced risk. It apparently means a positive score helps you save a lot of money, which is proven to be a smart financial move for you.

With good credit scores, you are able to unlock better loan options than people with poor credit. Also, you might receive a higher credit limit on a credit card. For example, good credit scores help you to take advantage of a low fixed-rate mortgage.

On the whole, building good credit scores is crucial for lower interest rates, the best credit cards, and long-term loans. You can also save your money by receiving rewards and better loan terms.

In addition, the above-mentioned information helps you to understand how to build credit scores with or without credit cards effectively and quickly. However, it is recommended to take advice from financial experts to build your credit history for long-term benefits.

To build your credit fast, you just need to:

You can get a 700 credit score in six months by avoiding new credit accounts, paying bills on time, adding your bills and utilities to credit bureaus, and reducing credit utilization.

As a beginner, you should become an authorized cosigner, apply for a secured credit card, consider a credit-builder loan, and have rental payments reported to credit bureaus. It helps you to build credit from scratch.

The 2 2 2 credit rule includes:

Sources:

How to Build Credit – MyFICO