A payroll tax plays a crucial role in funding essential government programs like Social Security, Medicare, and unemployment insurance. That’s why understanding what is payroll tax is important for both employers and employees.

Here, you can uncover the detailed information on its purpose, key components, calculations, examples, and the difference between payroll taxes and income taxes.

So, stay adherent to this article!

A payroll tax is an employment tax imposed on employees’ wages and salaries to fund government insurance like Medicare and Social Security. It consists of the Federal Insurance Contributions Act (FICA) tax, which the government uses to fund essential programs.

These taxes are split between employers and employees, with some portions withheld from workers’ paychecks while others are paid directly by the employers based on salaries.

This indicates that it plays a crucial role in funding Social Security, Medicare, and unemployment insurance.

Payroll taxes fund government programs such as Social Security and Medicare. The purpose of these taxes is to provide financial support to retirees, individuals with disabilities, or other survivors.

On the other hand, the Federal Unemployment Tax Act (FUTA) contributes to the unemployment programs, helping workers who have lost their jobs. Employees should submit Form W-4 when they are hired to have the withholding amount based on their salaries.

Note: The IRS (Internal Revenue Service) suggests that workers should submit Form W-4 every year to update their latest financial status because it affects their tax situation and business valuation.

Both employers and employees pay payroll taxes in the US. The fund is split between employers (7.65%) and employees (7.65%), meaning the total FICA rate is 15.3%.

It is important to note that employees fund their income tax obligations and contribute their share of FICA (Federal Insurance Contributions Act) taxes. At the same time, employers match employees’ FICA taxes and pay FUTA and state unemployment taxes, which are only funded by employers.

Furthermore, employers manage the administrative side by calculating employees’ withholdings, making deposits based on the payroll schedule, and evaluating tax liability and international tax. They also file monthly or yearly reports with the IRS.

Let’s look at this breakdown table to figure out the responsibilities of employers and employees.

| Employers’ Responsibilities | Employees’ Responsibilities |

|---|---|

| The FUTA (Federal Unemployment Tax Act) tax rate is 6.0% on the first $7,000 of taxable wages paid to each employee. | Fund federal income tax withholding based on Form W-4. |

| Matching employee contributions to FICA, such as 6.2% Social Security and 1.45% Medicare. | Contribute the employee portion to FICA, such as 6.2% Social Security and 1.45% Medicare. |

| Contributing to the State Unemployment Tax Act (SUTA) at rates determined by different states. | State income tax withholding from their paychecks (if applicable). |

| Additional Medicare tax (0.9% on income over $200,000). |

Also Read: How to Build Credit Fast: A Step-by-Step Guide for 2026

There are five types of US payroll taxes, including FICA taxes (Social Security & Medicare), Federal Unemployment Tax (FUTA), State Unemployment Tax (SUI), Income Tax Withholding, and Self-Employed Contributions Act (SECA).

Here are the following payroll tax and rate estimators in great detail.

The total taxable payroll is 15.3%, in which employees and employers contribute the same amount, i.e., 7.65%.

It is paid only by employers, generally 6% on the first $7,000 of an employee’s wages. Interestingly, it is often reduced to 0.6% if employers pay unemployment tax on time.

It is also paid by employers to state funds, helping workers who lose their jobs through no fault of their own. But rates may vary by state and are based on the employer’s experience rating.

In this payroll tax, employers are required to withhold federal and state/income taxes from employees’ paychecks and submit them to the IRS.

It acts as the self-employment equivalent of FICA taxes, covering both employers’ and employees’ funds. The total rate is 15.3%, comprised of 12.4% for Social Security and 2.9% for Medicare if the person earns $400 or more.

To calculate payroll taxes, you should evaluate an employee’s gross pay > taxable wages > withhold taxable income tax > FICA taxes > state and local tax > employer-only tax > net pay.

Let’s dig deeper into the following steps for in-depth guidance.

Step 1: Calculate Employee’s Gross Pay

Firstly, you should calculate the total earnings of an employee before taxes, including overtime, hourly wages, and bonuses.

Step 2: Determine Taxable Wages

Deduct contributions to plans such as 401(k), 403(b), 457(b) retirement plans, HSA, or Section 125 to determine taxable wages.

Step 3: Withhold Federal Income Tax (FIT)

Now, use the employee Form W-4 and IRS Publication 15-T to withhold federal income tax from an employee’s paychecks.

Step 4: Calculate FICA Taxes

Calculate 6.2% for employees and employers for Social Security from employee wages on the first $184,500. Also, evaluate 1.45% for employees and employers for Medicare insurance from employee earnings over $200,000 in a year.

Step 5: Evaluate State and Local Taxes

Apply the specific tax rates according to the state and locality laws to evaluate the state and local taxes.

Step 6: Compute Employer-Only Tax

Now, calculate FUTA (0.6% on the first $7,000 of each employee’s wages) and SUTA based on your assigned state law.

Step 7: Calculate Net Pay

At last, subtract all employee withholdings like FICA and income taxes from the gross pay.

Note: If you think that calculating payroll taxes can be challenging, you can hire professionals and opt for payroll services for your organization.

Also Read: New York Business Entity Search: A Master Guide for Establishing a New Business in New York

Let’s take a look at a detailed example of how to calculate payroll taxes.

For example, an employee’s annual salary is $60,000 ($2,307.69 gross per biweekly pay period) in a state with no income tax.

Single gross pay = $2,307.69

Employee Tax Withholdings

Total Employee Deductions = $185.00 + $143.08 + $33.46

$361.54

Net Pay = $2,307.69 – $361.54

$1,946.15

Employer-Paid Taxes

Summary of the payroll taxes:

| Category | Employee | Employer | Paid to the US Government |

|---|---|---|---|

| Federal Income Tax | $185.00 | – | $185.00 |

| Social Security | $143.08 | $143.08 | $286.16 |

| Medicare | $33.46 | $33.46 | $66.92 |

| FUTA | – | $13.85 | $13.85 |

| Total | $361.54 | $190.39 | $551.93 |

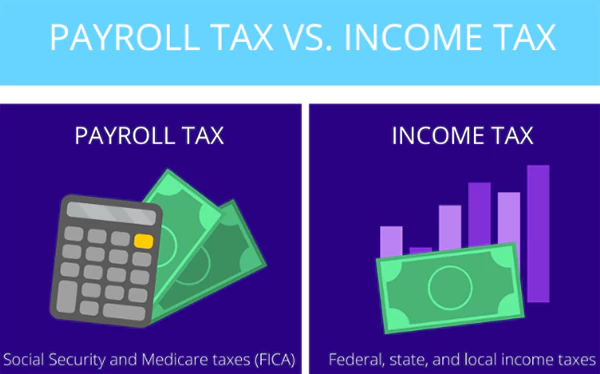

Payroll taxes are imposed on both employees and employers to fund Social Security and Medicare. On the other hand, income taxes are paid by individuals based on net earnings.

If you are still confused about the difference between both of them, let’s take a look at the breakdown table of payroll taxes vs income taxes.

| Feature | Payroll Taxes | Income Taxes |

|---|---|---|

| Purpose | Funds for vital government programs: Social Security and Medicare. | Funds for general government programs: defense, education, and infrastructure. |

| Who Pays | Split between employer and employee (7.65% each). | Paid by the employee and self-employed people (withheld by the employer). |

| Rate Type | Flat rate (15.3% total) up to wage base limits. | Progressive brackets (10% to 37%). |

| Calculation Base | Only wages, salaries, and bonuses. | Total income includes income, interest, and dividends. |

| Deductions | None | Reduced by deductions or credits (e.g., dependents). |

| Self-Employed | Pay the total tax rate (15.3%) as “self-employment tax.” | Pay based on net earnings. |

A payroll tax is only imposed to fund Social Security, Medicare, and unemployment insurance. It is different from income tax and is split between employers and employees, i.e., 7.65% each.

As a US citizen, you should be aware of what is payroll tax; otherwise, you can hire professional experts to calculate your payroll taxes and manage your financial decisions on your behalf.

Payroll taxes are the taxes paid by both employers and employees on wages, tips, and salaries, and funds to Social Security and Medicare.

Payroll taxes are levied to finance Social Security, Medicare, and the federal unemployment insurance program.

You should pay payroll taxes quarterly to the IRS by April 30, July 31, October 31, and January 31.

Taxes are calculated on a payroll by taking an employee’s gross earnings and pre-tax deductions and applying state and local tax rates.

Sources: