A bank statement is a financial document that shows all transactions that have been performed by an account over a certain time span. It offers information on deposits, withdrawals, payments, fees, and account balances, allowing individuals and businesses to monitor their financial activity.

These are also regularly used for loans, taxes, rents, and other financial procedures as evidence of financial activity.

Knowing how to review a bank statement and what it contains can help you get a better handle on your finances, especially when working with professional CFO services to improve financial planning and reporting.

- What is a Bank Statement?

- Why are Bank Statements Important?

- What Does a Bank Statement Include?

- Where Can You Get a Bank Statement?

- What is a Bank Statement Used For?

- Is a Bank Statement Acceptable as Address Proof?

- How Long Should You Keep Bank Statements?

- Bank Accounts vs Bank Statements: What’s the Difference?

- Types of Bank Statements

- Common Errors Found in Bank Statements

- Final Words

- FAQs

What is a Bank Statement?

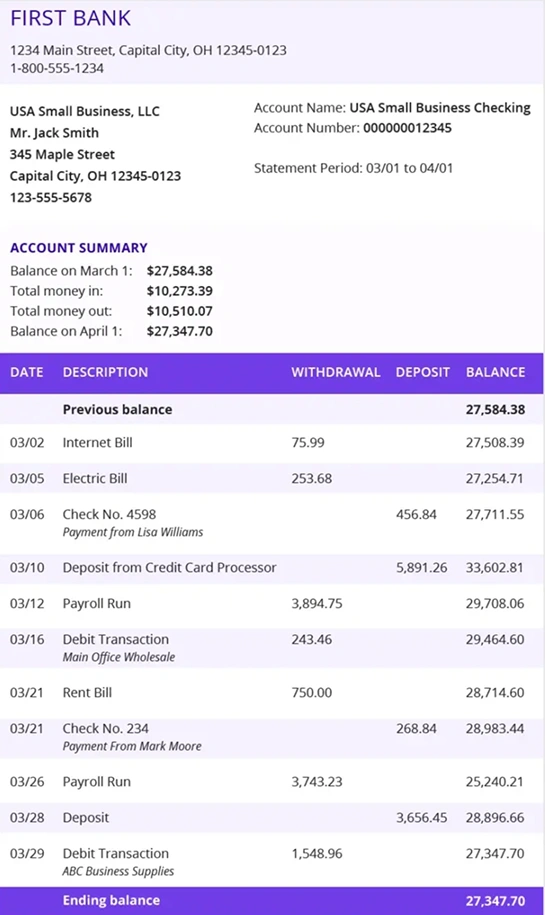

A bank statement is a document issued by the financial institution and includes every transaction made, balances, and account activity on the account for the indicated period.

It is a report of the account balance and shows the customers the status of the money that flowed in and out of their accounts.

A normal report will have:

- Account holder’s name

- Account number

- The time period

- Opening balance

- Deposits and credits

- Withdrawals and debits

- Fees

- Interest earned

- Closing balance

Most financial bodies issue these documents on a monthly basis, but reports can be issued for certain periods or dates upon request. Nowadays, many of them have digital statements that are available online and through mobile apps.

Why are Bank Statements Important?

The statement is significant as it enables people and businesses to monitor their finances, verify transactions, and keep accurate financial records.

These give account holders insight into the account’s activity and allow shareholders to make sound financial decisions.

- Keeping a Record of Income and Expenditure: One of the things that this document can help you with is understanding the source of your funds and where they are going. It’s good to review transactions periodically to become aware of your spending patterns and budgeting.

- Identifying Errors and Fraud: By reviewing the document, customers can identify any unusual transactions, incorrect charges, or unauthorized withdrawals. Early reporting of these issues can help avoid financial losses.

- Supporting Financial Applications: These reports are often required by organizations in order to ensure their financial stability. They might need to be used for loan applications, credit approvals, rental agreements, visa applications, income verifications, and maintaining financial records.

Bank statements are used by individuals and businesses to maintain orderly financial records for accounting, budgeting, preparing taxes, and ensuring accurate sales tax services compliance.

What does a Bank Statement Include?

A financial report contains information about accounts, transactions, account balances, fees, and other financial information on an account.

While some will have different formats in various banks, most will include the following information:

- Account Details: This section specifies the account and typically contains the account holder’s name, account type, account number, information, and date.

- Transaction History: The transaction section displays all of the activities within the account during the period. It may include deposits, ATM withdrawals, card payments, online transfers, and direct deposits.

- Balance Information: It is the responsibility of a statement to demonstrate starting balance, total credits, total debits, and ending balance. The closing balance is the balance that shows the amount available at the end of the cycle.

- Fees and Charges: Some of the fees that might be imposed are monthly account fees, ATM fees, overdraft charges, and service fees.

Where Can You Get a Bank Statement?

You can get the report via online service, mobile app, branch, or you can ask your account representative.

There are several ways to obtain a statement, such as:

- Online Banking: A large majority of banks provide their customers with a way to download statements via their online portals.

- Mobile Banking Apps: Numerous applications will offer instant access to digital statements.

- Branches: Customers may stop by one of the branches and pick up print copies.

- Customer Support: The statements can also be obtained by customers via customer service.

What is a Bank Statement Used For?

These documents serve as a record of financial activity, a record of managing the finances, and proof of transactions or income.

Common uses include:

- Loan Applications: Financial statements might be required to assess financial stability by lenders.

- Rental Applications: Landlords can check if they would like to verify income and payment ability with statements.

- Tax Purposes: Statements are used to organize business and personal financial records, while also supporting accurate bookkeeping and payroll services for businesses.

- Budget Planning: It is beneficial to take a look at reports to discover how money is being spent and where it can be saved.

Is a Bank Statement Acceptable as Address Proof?

As these reports generally include the account holder’s name, address, and account records, you can use them as your proof of address.

These are the official documents provided by the financial institutions, and all the other companies and institutions accept them.

However, the requirements differ, and some organizations may require a statement from a recent month or a particular format.

How Long Should You Keep Bank Statements?

The reports should be retained for as long as necessary for financial records, tax, or legal purposes. However, in general it is recommended to keep the records for 3-4 years and even 5 years if you are required to maintain a longer financial history, particularly for a loan, investment, or tax payment.

People can retain statements to:

- Track spending

- Review past transactions

- Resolve disputes

Statements are kept longer by businesses for:

- Accounting

- Audits

- Tax reporting

- Supporting business valuation services during mergers, acquisitions, funding, or strategic planning.

The digital copies will be stored securely for future access.

Bank Accounts vs Bank Statements: What’s the Difference?

The money is stored in an account, and the report is the document that shows the transactions that have been conducted on that account.

Although the two are linked, they are used for different purposes.

| Bank Account | Bank Statements |

|---|---|

|

|

Check Out: Inheritance Tax: Who Pays It, Common Mistakes, and Importance

Types of Bank Statements

There are various types of statements for business, personal, electronic, and credit cards. Each type has its own purpose in regard to the account and financial activity.

1. Personal Bank Statement

A personal one is a bank statement issued to an individual for their personal checking or savings.

It helps individuals to record the following:

- Salary deposits

- Personal expenses

- Transfers

- Savings activity and investment deposits, such as 401 (k).

2. Business Bank Statement

A business documents the business transactions that have occurred in a company’s account.

- Monitor cash flow

- Track expenses

- Prepare financial reports

- Reconcile accounts

3. Electronic Bank Statements

An electronic statement, also called an e-statement, is a digital statement delivered electronically.

Customers have access to it via:

- Online service

- Mobile applications

- Email services

4. Paper Bank Statement

A paper statement will be printed by the financial institution. Although not as popular today, some people still want a hard copy for their files.

5. Credit Card Statement

The information on a credit card statement includes information about the credit card account, such as:

- Purchases

- Payments

- Interest charges

- Outstanding balance

Common Errors Found in Bank Statements

Errors on statements include inaccurate changes, deposits that are missing or unrecorded, duplicate payments, or unauthorized payments.

Some issues to look for include:

- Unauthorized Transactions: Any transactions or transactions that have been made without you being aware of them could be a sign of fraud.

- Incorrect Fees: It sometimes do not charge properly.

- Missing Deposits: Processing delays may cause a deposit not to show up.

- Duplicate Charges: A payment can be inadvertently made more than once.

Notify your financial lender if you notice any mistakes as soon as possible.

Final Words

A bank statement is a crucial financial record that aids individuals and organizations in comprehending their transactions. Regular review of statements allows account holders to monitor spending, detect errors, deter fraud, and control finances.

Knowing how bank statements work can make savvy financial decisions for anyone, whether they are managing their own finances or those of a business, including organizations handling cross-border operations with the help of international tax services.

Read Next: Going Concern Assumption: Meaning, Principle, Examples, and Importance in Accounting

FAQs

How do I get a bank statement?

You can get it by logging into your bank’s online banking portal or mobile app or by visiting a bank branch. Typically, you can download or request statements at any time from most banks.

What is a bank statement?

It is a report that displays your bank activity, such as a bank balance at a certain time, withdrawals, payments, fees, and deposits.

How do I download a bank statement?

You can download it by logging on to their online banking account and then selecting their bank account and the statement or e-statement option.

Can I see my bank statement?

You can view your report via online banking, your bank’s mobile app or ask your bank for a copy.

Can I get a bank statement immediately?

Yes, most banks offer instant access to their digital report via online banking or their mobile app once the statement period has been released.