The most significant financial statement that a business uses to gain insight into its income and losses is a profit and loss statement. It indicates the result of the company’s profit or loss for a particular period.

A P&L statement helps you understand how your business is performing, manage costs, make sound business decisions, and determine when growing companies may benefit from CFO services. Let’s get into depth with profit and loss statements in this blog!

- What is a Profit and Loss Statement?

- Why is a Profit and Loss Statement Important?

- What does a Profit and Loss Statement Include?

- How Does a Profit and Loss Statement Work?

- How to Prepare a Profit and Loss Statement?

- What is the Difference Between a Profit and Loss Statement and a Balance Sheet?

- When to Review a Profit and Loss Statement?

- Common Errors to Avoid in the Profit and Loss Statement

- Final Words

- FAQs

What is a Profit and Loss Statement?

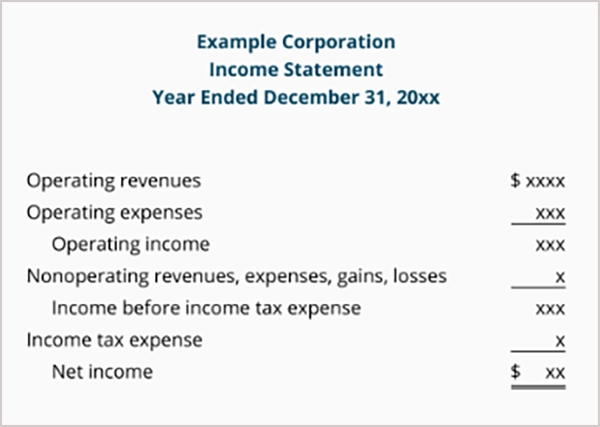

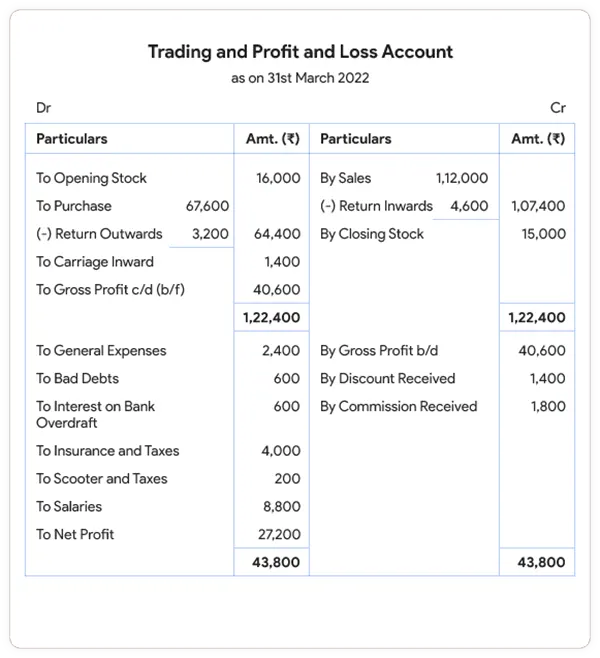

The profit and loss statement provides a snapshot of a business’s income and expenses, and its profits or losses, over a particular period.

Also known as an income statement and profit and loss statement, this report provides a clear picture of how much money a business earns and spends. It will aid business executives in determining if their enterprise is turning in adequate earnings to be profitable.

It is typically created on a monthly, quarterly, or annual basis. By reviewing this report regularly, businesses can get ahead of potential problems and identify financial trends.

The basic equation of the P&L statement is:

Profit or loss = Revenue – Expenses

As long as expenses are lower than revenue, the business makes a profit. When expenses are greater than income, the business makes a loss.

Why is a Profit and Loss Statement Important?

It is crucial to have a profit and loss statement because it shows a business’s financial performance and aids decision-making for the future. Businesses use the statements for several reasons, such as:

- Track Business Profitability: A P&L statement will tell you if your business is profitable once you’ve factored in all costs. It enables you to know whether your pricing, selling, and spending methods are working or not while also helping you evaluate whether your company is ready for a business valuation.

- Identify Financial Trends: Businesses can identify revenue gains and losses, rising costs, or falling profits by using profit and loss statements from different time periods.

- Make Smarter Decisions: P&L information can be utilized by business managers to determine the necessity to cut expenses, change pricing, grow the business or invest in it.

- Support Loan and Investment Applications: Financial statements, such as P&L, are frequently analyzed by lenders and investors to assess the assets and liabilities and financial strength of a company.

- Prepare for Taxes: Good income and expense records are important to make it easier to prepare taxes comply with sales tax requirements, and allow businesses to report income accurately.

What does a Profit and Loss Statement Include?

A profit and loss report records all the primary sources of income and expenses that impact a business’s profitability.

While the format may differ, a typical P&L’s definition includes these sections:

1. Revenue or Sales

Revenue is the money a business generates from sales of its product or service. It is typically the top line of a profit and loss statement and is the company’s total revenue prior to any expenses being applied.

A firm can have a combination of, for instance, the following:

- Product sales

- Service income

- Subscription revenue

- Other business earnings

2. Cost of Goods Sold

The amount of money that a company spends to produce a product or service. Cost of goods sold is the actual expense of producing or providing a product or service.

Examples include:

- Raw materials

- Manufacturing costs

- Direct labor

- Packaging expenses

You must subtract COGS from revenue to get the gross profit.

3. Gross Profit

Gross profit is the profit which is obtained after deducting the direct production cost.

Gross Profit = Revenue – Cost of Goods Sold

The company’s gross profit is typically high if they are well-managing their production costs.

4. Operating Expenses

Operating expenses are the continuing costs that have to be maintained to keep a business going.

Typical common operating expenses are:

- Rent

- Salaries

- Marketing costs

- Utilities

- Software expenses

- Insurance

- Office supplies

5. Net Profit or Net Loss

Net profit is the profit after any deductions, taxes, and other costs are subtracted.

If it is positive, then the company has a net profit. If it is negative, then it is a net loss.

Check Out: What Is Stagflation? Meaning, Causes, Effects, and Examples

How Does a Profit and Loss Statement Work?

The accounting principle of a P&L statement is to use the income and expenses statement to determine the overall performance of a business.

The profit loss statement is laid out in a straightforward way:

- The revenue needs to be recorded first.

- Then, direct costs are deducted.

- Gross profit is determined.

- Deductions are made for operating expenses.

- Final profits or losses are calculated.

A business, for instance, may have a revenue of $100,000, but its expenses total $70,000, leaving it with a profit of $30,000.

Regularly checking these numbers lets companies know where money is coming from and where it’s going.

How to Prepare a Profit and Loss Statement?

A profit & loss statement can be compiled by listing your financial records for a period of time.

Follow these steps:

- Select a Reporting Period: Choose to make an annual, quarterly, or monthly P&L statement.

- Calculate Total Revenue: Include all income from sales, services, and other income.

- List Business Expenses: Take note of all expenses, such as operating costs and direct costs.

- Calculate Gross Profit: Determine the profit after subtracting the cost of goods sold from the total revenue amount.

- Work Out the Net Profit or Loss: Calculate the net profit by deducting out all the other costs from gross profit.

A lot of businesses have accounting software that will automatically produce profit and loss reports based on what they have recorded.

What is the Difference Between a Profit and Loss Statement and a Balance Sheet?

A profit & loss statement is used to see the performance of any business over a period of time, whereas a balance sheet is used to see the financial position of any business at a particular point in time.

A statement of a P&L is directed at

- Revenue

- Expenses

- Profit or loss

A balance sheet mainly contains the following:

- Assets

- Liabilities

- Owner’s equity

These financial statements provide a comprehensive picture of a company’s finances.

When to Review a Profit and Loss Statement?

Every business should regularly analyze its profit and loss statement to keep track of the financial changes and then make the best decisions.

Small businesses might consider monthly P&L reports, whereas larger businesses might look at the reports weekly or quarterly.

Regular audits are beneficial for businesses because:

- Catch unnecessary expenses.

- Monitor the revenue changes.

- Improve the budget tracking and allocations.

- Plan the future strategies.

It will be more difficult to address financial problems if you wait until the end of the year.

Common Errors to Avoid in the Profit and Loss Statement

By steering clear of the common pitfalls in the P&L, businesses can ensure that their financial records are accurate and that they are making the right decisions for their business.

Here are the common errors:

- Blending Personal and Business Expenses: Always avoid mixing personal and business transactions. It will mess up the records completely.

- Recording Expenses Incorrectly: If the expenses are misclassified, it can lead to incorrect profit figures.

- Ignoring Small Costs: You must note down even the smallest payments, as the little things can add up and impact profits.

- Failure to Regularly Update Statements: Older reports may not accurately reflect the current state of the business.

- Forgetting Non-Cash Expenses: Items like depreciation can impact profitability and should be included.

Read Next: Top Hedge Funds in the World: Rankings, Strategies, and Insights

Final Words

A profit and loss account is a vital financial statement that aids companies in knowing their revenue and expenditures and their profitability by providing a clear overview of the financial transactions that have occurred within a business during a particular time interval.

Regularly checking a P&L statement allows businesses to make well-informed decisions, control spending, and plan for future expansion. Whether created manually or through accounting software, an accurate profit and loss statement provides valuable insights into a company’s financial health.

FAQs

What are the key components of an income statement?

The main components of an income statement are revenue, cost of goods sold, gross profit, operating expenses, taxes, and net profit or loss.

What is the primary purpose of an income statement?

An income statement is intended to provide information on a company’s financial performance over a period of time, including its income, expenses, and profitability.

What are the different formats of an income statement?

There are two types of income statements: single-step and multi-step. Profit is calculated in a single step by single-step statements and in multiple steps by multi-step statements.

How to read and interpret an income statement?

An income statement is read by looking at revenue, expenses, profit margins, and net income to determine if the business is making a profit or not.

How does an income statement relate to other financial statements?

An income statement is used in conjunction with the balance sheet and cash flow statement to give a complete picture of the financial position of a business.

Sources:

What Is a Profit and Loss (P&L) Statement? Definition, Types, and Analysis – By Oracle NetSuite

What is a profit and loss statement? – By Xero